by Dr. Michael Sklarz*, Dr. Norman Miller** and Dr. Anthony Pennington-Cross*** | January 7, 2019

Download a PDF file of this research paper here.

Introduction

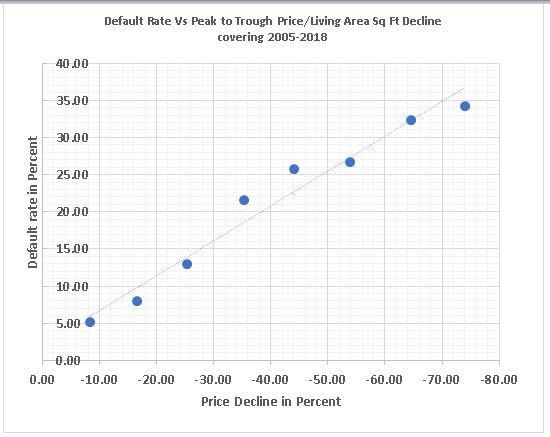

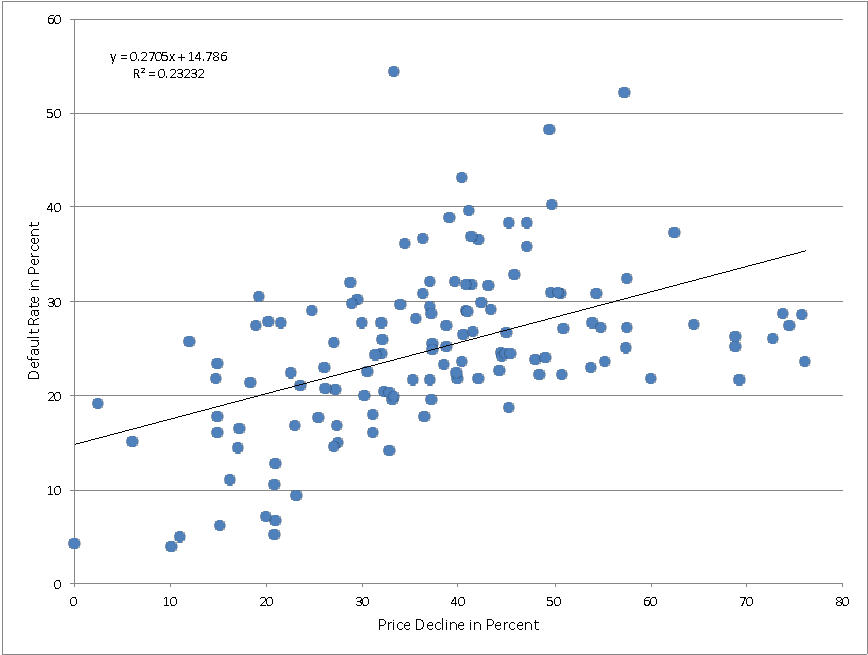

In early December of 2018 we published a discussion on the significant and dominant influence of price trends on mortgage default rates. There we noted that home price changes, analyzed at the zip code level, were a significant driver of default rates and were especially dominant when the loan to value ratios were relatively high. Here, we continue the analysis using the change from the peak to the trough of prices over the period of 2005 through 2018 for a variety of CBSAs. Again, we see a very strong impact on residential mortgage backed securities (RMBS) default rates from average property price declines. For the aggregate of all of the zip codes in all of the CBSAs shown below, we see a correlation between the default rate and peak to trough price decline of -0.74. We show all of these markets in aggregate in Exhibit 1 below with a trend line inserted. Default rates climb significantly when peak to trough prices decline more than -20%. This is consistent with typical loan to value, LTV, ratios and shows why conservative loans will be at 80% LTV or below.

Exhibit 1: Aggregate Default Rates Vs Peak to Trough Price Change for the Orange County, Los Angeles, San Diego, San Francisco and Seattle CBSAs Grouped in Deciles

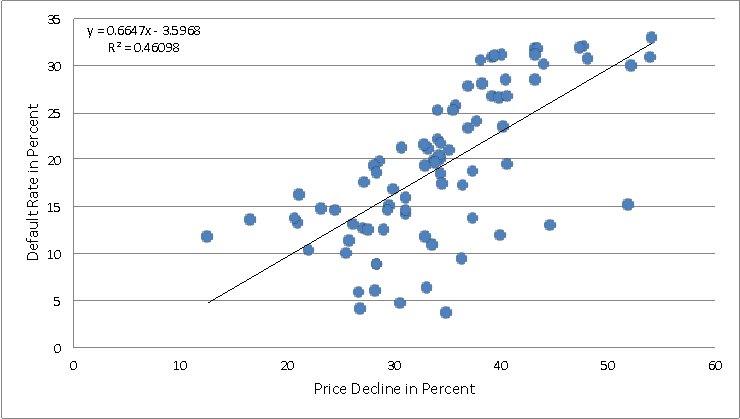

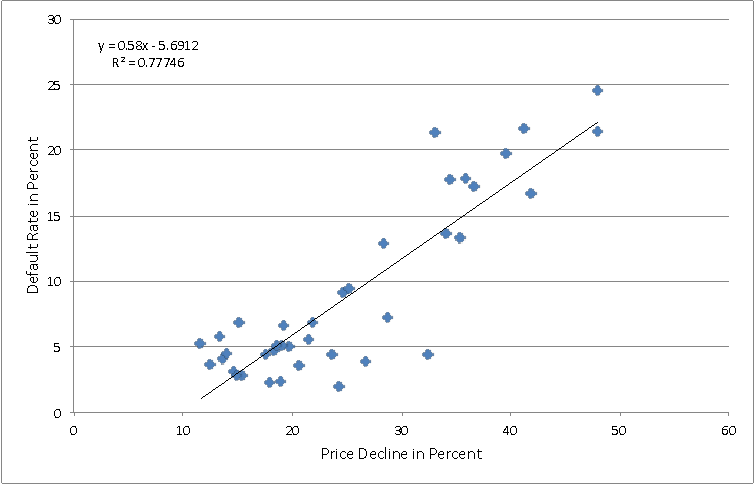

Exhibit 2: Zip Code Default Rates Vs Peak to Trough

Price Change for the Orange County CBSA

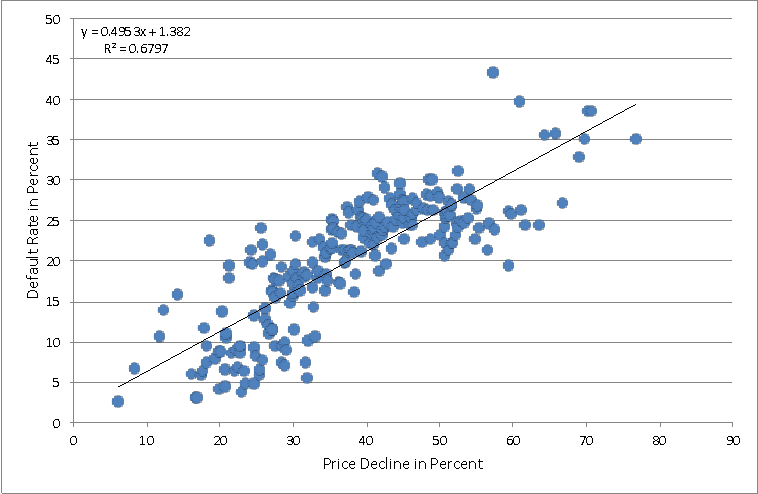

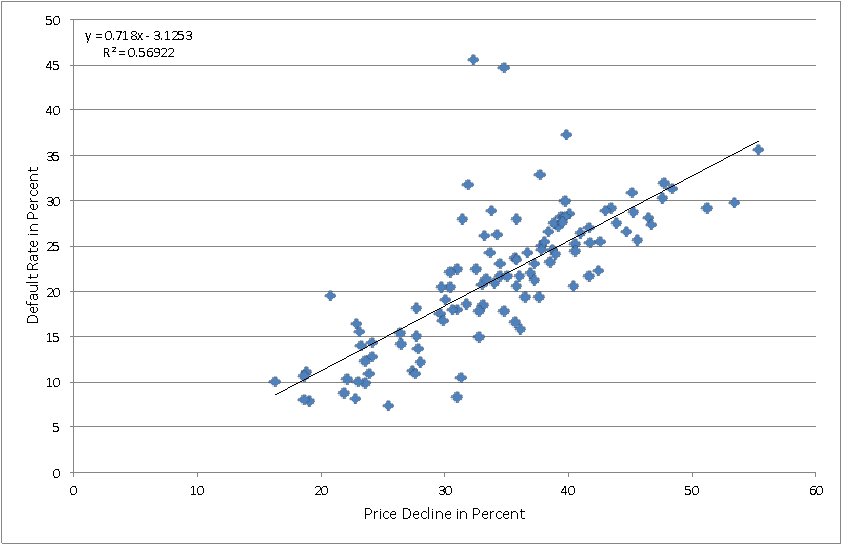

Exhibit 3: Zip Code Default Rates Vs Peak to Trough

Price Change for the Los Angeles CBSA

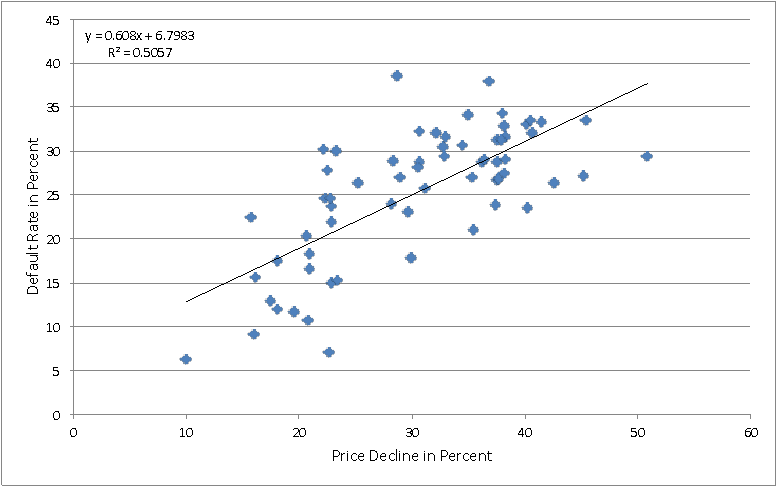

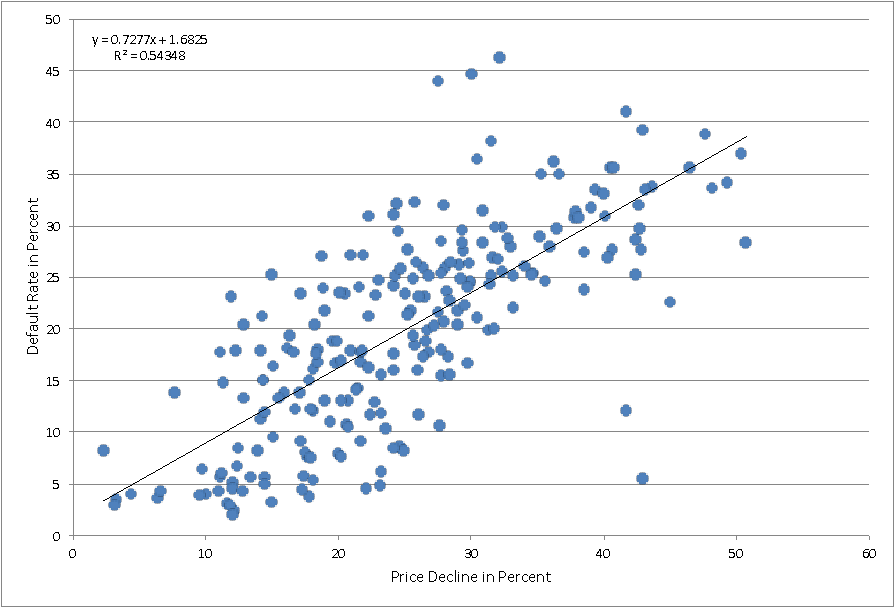

Exhibit 4: Zip Code Default Rates Vs Peak to Trough Price Change for the San Diego CBSA

Exhibit 5: Zip Code Default Rates Vs Peak to Trough Price Change for the San Francisco CBSA

Exhibit 6: Zip Code Default Rates Vs Peak to Trough Price Change for the Seattle CBSA

Exhibit 7: Zip Code Default Rates vs Peak to Trough Price Change for the Boston CBSA

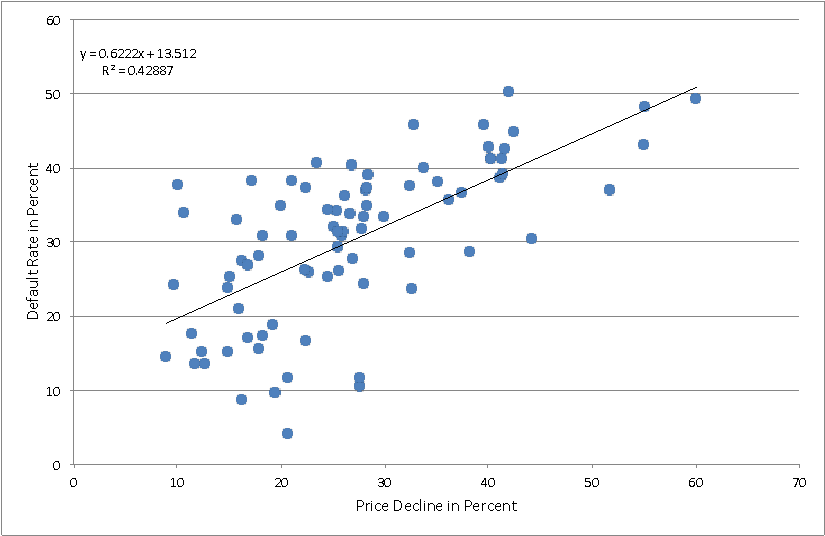

Exhibit 8: Zip Code Default Rates vs Peak to Trough Price Change for the Charlotte CBSA

Exhibit 9: Zip Code Default Rates Vs Peak to Trough Price Change for the Washington DC CBSA

Conclusions

House prices matter to almost everyone, ranging from towns and their homeowners to mortgage backed securities investors. Buyers who buy at a peak of the price cycle and subsequently face significant price declines are much more likely to default, regardless of personal circumstances with respect to employment, life trigger events, or credit rating status. Equity cushion is a critical element in default forecasting models, along with accurate valuations at the time of purchase and mortgage underwriting. Here we show that the impact of price declines on default rates is very strong and consistent across a variety of different locations and corresponding home price levels.

*Collateral Analytics CEO

**University of San Diego School of Business and Collateral Analytics Research

***Marquette University College of Business and Collateral Analytics Research