by Dr. Michael Sklarz* and Dr. Norman Miller** | May 01, 2019

Download a PDF file of this research paper here.

Preface: At first glance it might seem that raising the limit for home mortgages requiring appraisals would force a drastic change on the industry. It certainly covers a lot more homes in the US, in fact, nearly everyone. But the proposals to raise the limits for requiring traditional appraisals cover only a portion of existing home mortgages, and simply raising the threshold for appraisal will not result in a revolution towards more efficiency in the mortgage industry; that requires some policy changes to deal with the reality that value estimates are not 100 percent certain at any single point estimate.

Introduction

On February 5th of 2019 the Mortgage Bankers Association sent a letter to the US Comptroller of the Currency, the Chairman of the Federal Reserve Board of Governors and the Chairman of the FDIC, supporting proposals to eliminate manual appraisals from the mortgage underwriting process, when mortgages are $400,000 US dollars or less..[1] Currently the threshold for requiring manual appraisals is $250,000. Specifically the MBA stated “MBA supports the agencies’ desire to raise the threshold for appraisal exemptions as a means of leveraging technology to better serve consumers, while also preserving crucial safety and soundness standards.” They go on to say “given the significant improvements in the development of automated valuation models in recent years, the tools and resources available for the required alternative evaluations are significantly enhanced compared to 1994. As a result, we believe the proposal is not a threat to safety and soundness. … Consumers may also benefit from an increase in the exemption. In the current market, the lengthy processing times and high costs often associated with traditional appraisals reduce the efficiency of the loan origination process. … Allowing banking institutions to expand their use of alternative evaluations will help offset the effects of appraiser supply shortages, reducing costs and shortening (or eliminating) delays that have occurred in many markets. More broadly, raising the threshold will create a more efficient residential mortgage market for lenders and consumers by expediting valuations and lowering closing costs.”

The above statements make it appear that a broad swath of the market would be exempted from traditional appraisals, but this is not the case. According to a John Russell discussion in 2018, “An FRT (Federally Related Transaction) is a mortgage loan whose total amount is above the $250,000 threshold, is not insured or guaranteed by a federal agency, and is not sold or contemplated for sale to a GSE such as Fannie or Freddie” covering approximately 8 to 12% of the mortgage market.[2] Still, there are solid reasons why traditional appraisal has come under fire since the last housing crisis and we address some of these issues here, as well as speculating on the question of how many homes are in fact, above an applicable threshold in price, to possibly be exempt under FRT.

As we have said often in past discussions on the risk metrics used in the mortgage industry, the appraisers are not at fault for a system that rewards upwardly biased appraisals.[3] It is the system itself, where lenders want loans approved which are most often sold to mortgage investors. Mortgage originators are not at risk should default occur.[4] This same system has suppressed appraisers and inhibited the appeal of a career in appraisal for aspiring valuers.

Traditional appraisal here refers to human driven appraisals, that include 1) identifying comparable properties within an appropriate neighborhood, 2) adjusting these towards the subject property to answer the question; “what would the comparable property sell for if it was more like the subject property?”; and 3) concluding a point value estimate for the subject property. This process is labor intensive, requires field research, has many places for human judgement and is ideally performed by an appraiser familiar with the neighborhood of the subject property. Traditional appraisals are costly, require significant time, and have been required by mortgage lenders for decades. When performed by competent appraisers that can ignore the pressures to hit the mark (hit a certain price) they can effectively protect home buyers from over paying and mortgage investors from undue risks.

If Not Traditional Appraisals then What?

Automated valuation models, AVMs, along with property condition reports will still be required in the underwriting process, even if traditional appraisals are not required. AVMs perform the same tasks as humans but can process more data, systematically adjust for differences from comparable properties to the subject property and by way of design, hit the most probable price as an estimate of value. AVMs express values with low-high price ranges and confidence metrics. This is useful information for mortgage underwriting, as the larger this range the less certain is the point value estimate.

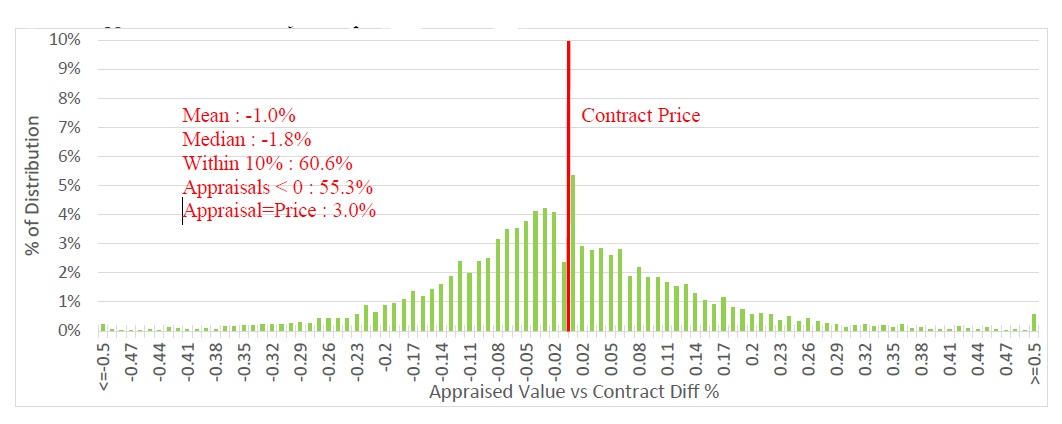

AVMs value estimates will be fairly evenly distributed above and below contract prices, similar to the results we observe when appraisers are not told the contract price. An interesting study provided such a comparison. See Exhibit 1 below where traditional appraisals were run and compared to subsequent contract prices, where the contract prices were unknown.[5] Note that roughly half of the value estimates are to the right and the left of the subsequent contract price. We do see a mean difference in the estimates versus contract prices of -1.0% and this is a result of some people over paying, relative to market value for this particular sample.

Exhibit 1: Appraisal Estimates Versus Unknown Contract Prices

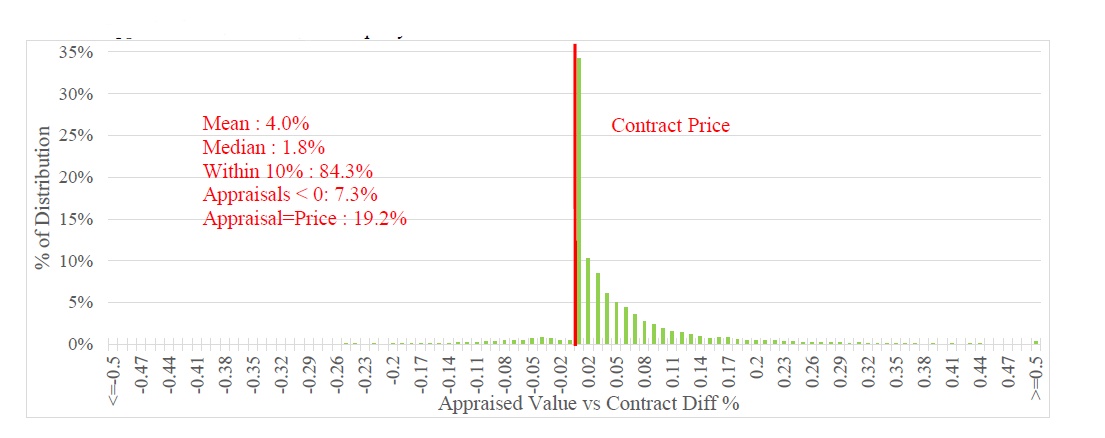

Exhibit 2: Traditional Appraisals Versus Contract Prices, Where Contract Prices are Known

The manual traditional appraisals, where contract prices are known by the appraisers, for this same sample are shown in Exhibit 2 and average 3% above the average contract price. Note that nearly all of the appraisals are at or above the contract price.

Some appraisers are embracing interactive AVMs that allow fast efficient and automated valuation to be driven by local experts. This will increase the productivity of the appraisers who use these tools, but also force others from the industry. Yet, the use of AVMs, when driven by a human, does not necessarily eliminate the problem of pressure from lenders to hit a certain price. This is why most lenders use traditional appraisal methods, even though 68% of all homes are under $312, 500 the typical threshold for a $250,000 mortgage, and eligible for automated appraisal methods combined with inspections on property condition.

AVMs are much improved over the state-of-the-art in the 1990s and early 2000s, and one reason they are favored by mortgage investors, including Fannie Mae and Freddie Mac, is that AVMs are agnostic about hitting a certain value estimate. We see this from a study covering millions of mortgages by Calem, Lambie-Hanson and Nakamura (July, 2017) from the Federal Reserve Bank of Philadelphia. Calem et al conclude the current system of price disclosure (to appraisers) creates a flaw in the risk management system. They suggest that when appraisals exactly hit the purchase prices, or refinance target price, as is so often the case, no real information is gained by lenders and that “…we find that appraisals are less predictive of default than automated valuation model estimates.” Some 30% of all appraisals in the Calem et al study were exactly equal to the purchase prices and over 92% were at or above the contract price.6 Several other studies discuss upward appraisal bias and the problem this poses for objective mortgage risk analysis, i.e. Cho and Megbolugbe (1996), Agarwal, Ben-David and Yao (2013) or Griffen and Maturana (2014) among others.

Such studies reveal why the MBA and mortgage investors are not opposed to eliminating traditional appraisals. Again, this is not to say that appraisers are not competent, but the system does not reward competency as much as facilitation of lenders desiring loan approvals.

How many US houses fall within the new proposed guidelines for requiring manual appraisals?

Using a loan to value ratio of 80% with a $400,000 mortgage we generate a price of $500,000 as a reasonable benchmark. What percentage of US homes exceed this value? The answer is about 19.4% based on MLS (Multiple listing service) sale transactions and about 14.6% based on public records.

Another way to look at the proportion of homes that fall under $500,000 is via this graph shown in Exhibit 3, which includes second quarter 2019 AVM value estimates for nearly all of the US including both single family and condominium units. The small fonts may be a bit hard to read, but the $500,000 mark starts around the middle of the horizontal axis with the change in column color to red. While the red column portion represents 14% of all homes, many of these buyers use lower loan-to-value mortgages as they are on their second, third or fourth homes where loan to value ratios are typically much lower. Also shown in Exhibit 3 is a black column line equal to $312,500 in price. All those homes to the left of this line, 68% of the distribution, are generally eligible for automated valuations.

Exhibit 3: Distribution of Value Estimates for both condos and single-family homes

When sorted by the average single-family selling prices in 2018 by state, only three states/districts exceed

$500,000. These are Hawaii, California and the District of Columbia. Massachusetts is close at $489,000 and the rest are well below $500,000 in average selling price. See Exhibit 4 for the percentage of homes that are at $500,000 or below by state for the second quarter of 2019.

Exhibit 4: Percentage of Homes Below $500,000 By State

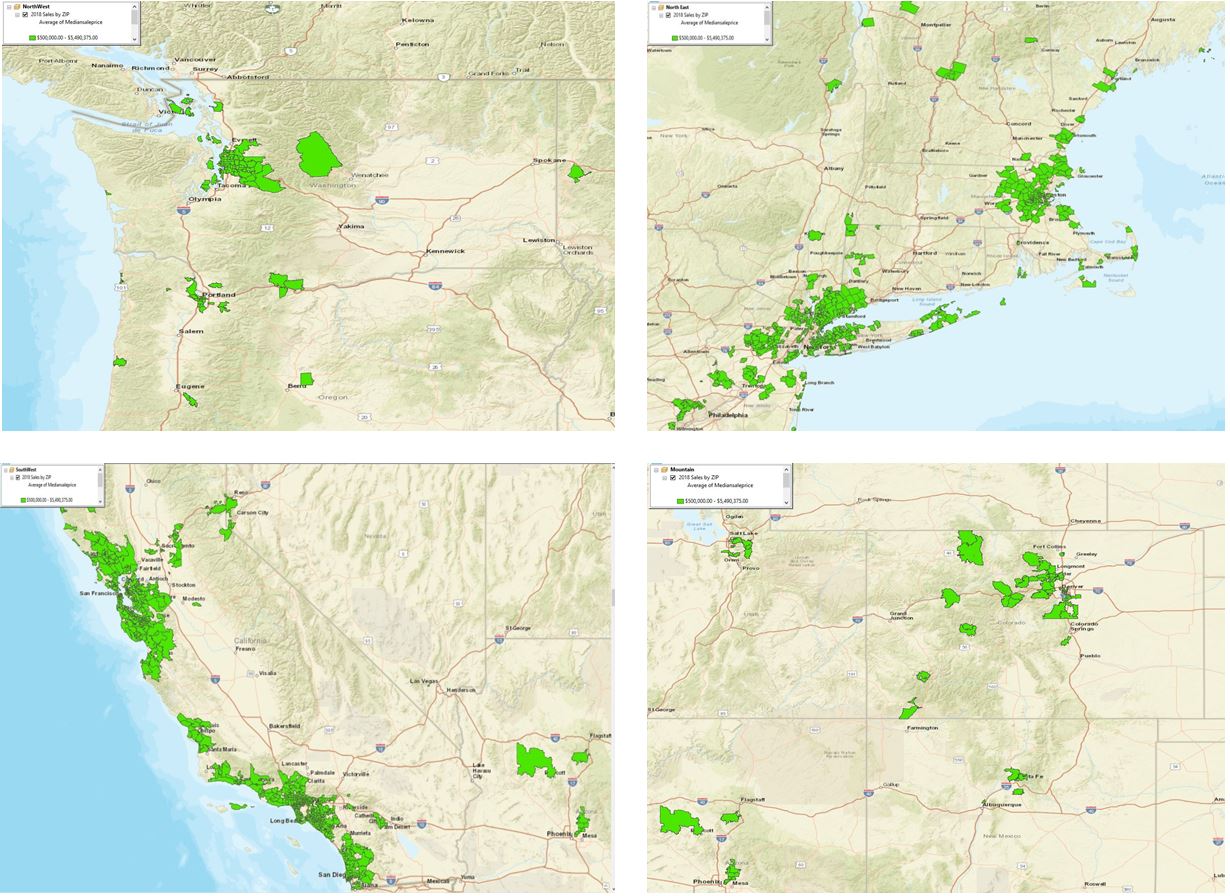

When sorted by zip code, approximately 6.0% of all zip codes have average prices in 2018 exceeding $500,000. A Number of these are mapped below in Exhibit 5 and shown as green. Naturally, it is the high home price markets of the California coast, along with various high-priced markets in Washington, Colorado, and the Northeast US where the $500,000 mark is typically exceeded. Again, in many of these markets we find home owners with much lower than average loan to value ratios, so many of these homes could also be eligible for the new proposed appraisal guidelines. Not shown is Hawaii, where obviously there are a number of zip codes where prices exceed $500,000. Still, it becomes obvious that a small part of the US geography will fall over $500,000 for average selling prices and more than 85% of all households will, if the proposal moves ahead, be eligible to speed up the valuation process, without significantly impacting the risk of default for lenders. Yet, most lenders will continue to utilize manual appraisals, not because of accuracy, but because of the fear that the appraisal values will come in below contract prices. This suggests that raising the threshold from $250,000 to $400,000 will have little impact on the demand for appraisers, but it also suggests systemic problems with the current underwriting policies. What is essential is recognition that value estimates are a range, and lenders need to be able to account for value uncertainty.

Exhibit 5: Map of Zip Codes Where Average Prices in 2018 Equal or Exceed $500,000

Conclusions

The move to eliminate traditional appraisals, from even a modest subset of residential mortgages, is a baby step in modernizing the regulation and underwriting process for home buyers, but it is not a sufficient one. Increasing the use of AVMs will create some underwriting problems in that nearly half of the AVM values will be below contract prices, not because the homes are not worth what someone decides to pay, but rather because we know that all real estate has a low-high range over which it might contract and there is uncertainty in point value estimates.

Two more steps are needed to modernize the mortgage underwriting process, including 1) applying the exemption to a larger set of mortgages when appraisal confidence is reasonably high, and 2) to recognize that there is really a range of values for each property and if the contract prices fall within that range, yet to be defined by policy makers, then it is an acceptable risk for lenders and mortgage investors. Appraisers know there is uncertainty in their point value estimates, but have not been required to disclose a range within which they are confident. Such disclosures should be based on a statistical process and appraisers may need additional training in order to incorporate the addition of high-low property value estimates into a report.[7] Encouraging such disclosure and market value uncertainty metrics would be very useful for loan underwriting.

When AVMs are used, lenders could consider engaging an experienced appraiser when the uncertainty surrounding the AVM driven value estimate, or the high-low estimate as a percentage of price exceeds some minimum level. For example, when the low range estimate at 80% confidence is more than 7.5% below the contract price, the lender may wish to engage an appraisal to review the low side estimate. If the low side estimate suggests a loan-to-value ratio above some threshold, perhaps 80%, then the approved loan amount may need to be reduced. Alternatively, loans on properties where value is less certain could add in a risk premium to the interest rate charged to account for additional risk.[8]

Without new mortgage underwriting policies, too many mortgage applications would be rejected based on lower than contract price AVM driven appraisals. This is not to say that traditional appraisals are better for mortgage risk analysis. Point estimates, without information on the variance and uncertainty behind the appraisal have always been problematic for the mortgage industry. AVMs at least provide information on this uncertainty and at the same time, this additional information is not currently used in the underwriting process. A policy to use both the uncertainty behind the appraisal estimate, no matter how generated, and the point estimate of value based on most probable price is essential, before lenders will likely embrace an increase in the use of automated valuation systems, but we expect that day will come.

*Collateral Analytics CEO

**University of San Diego School of Business and Collateral Analytics Research

Footnotes

[1] See 83 FR 63110, “Real Estate Appraisals,” December 7, 2018. Available at: https://www.federalregister.gov/documents/2018/12/07/2018-26507/real-estate-appraisals.

[2] See http://www.appraisers.org/docs/default-source/discipline_rp/watering-down-of-frts_0218.pdf?sfvrsn=2

[3] For one of many papers that discuss this upward bias, see “Contract Price Confirmation Bias: Evidence from Repeat Appraisals” by Eriksen, Fout, Palim, and Rosenblatt, Oct. 28, 2016, Fannie Mae working paper.

[4] “Skin in the game”, a Dodd Frank proposal, was supposed to eliminate this lack of risk bearing by originators, but 80% loan to value mortgages are generally exempted from any risk bearing by mortgage originators. See Whatever happened to Skin in the Game? By Steve Cook Aug. 22, 2016 https://www.inman.com/2016/08/22/what-ever-happened-to-skin-in-the-game/

[5] Taken from the study by Eriksen, Fout, Palim, Rosenblatt, referenced in footnote 2

[6] See Working paper No. 17-23 by Calem, Lambie-Hanson and Nakamura, Federal Reserve Bank of Philadelphia

[7] See “Appraisal Accuracy and Confidence Scoring” Oct. 30, 2017 at https://collateralanalytics.com/news- research/page/5/

[8] “Collateral Analytics featured in Appraisal Buzz: Adjusting Loan to Value Ratios to Reflect Uncertainty” Aug 22, 2016 at https://collateralanalytics.com/news-research/page/7/